Five Myths About Bankruptcy

When facing financial desolation, it’s hard to think straight, you are so gripped by worry. Bankruptcy plays into many people’s doomsday scenarios, imagining that it will be the end of them financially and personally, as family relationships are ripped apart under the strain.

When facing financial desolation, it’s hard to think straight, you are so gripped by worry. Bankruptcy plays into many people’s doomsday scenarios, imagining that it will be the end of them financially and personally, as family relationships are ripped apart under the strain.

The truth is, bankruptcy and consumer proposals are about getting control back over your life and feeling relief as you take steps towards recovery. As soon as bankruptcy is filed, the calls from creditors begin to stop and an immediate stay of proceedings means that none of your assets can be seized, other than those signed over in security in case of default.

The immediate emotional and financial relief can relieve the enormous burden on a family and actually repair the relationships of frazzled spouses.

Here are five myths that many people hold about the bankruptcy process:

1. Everyone is going to know that I am a deadbeat.

Though bankruptcy is a public proceeding it isn’t publicized. So even though there are sections in the newspaper devoted to bankruptcy notices aimed at alerting creditors, these only involve large or corporate bankruptcies. The only way your neighbours and friends would know that you are going bankrupt is if you tell them or they decide to go to Office of the Superintendent of Bankruptcy’s website, register as a user and pay an $8 search fee to find you. The chances of this happening are small to none at all.

2. I will never get credit again

Again, not true. A first-time bankruptcy is usually a nine month process. When the process is finished, you are free of previous debt and financial obligations, there are many companies eager to lend you money again. Some people can even get a loan or secured credit card while they are bankrupt. If you are like most people, you can start rebuilding your credit rating right away by getting, for example, that secured credit card. You may qualify for a mortgage or car loan in a few years. Here are five ways you can rebuild your credit.

3. I will lose everything I own.

Contrary to popular belief, you don’t lose all your assets when you go bankrupt. There may be some things you will have to give up, especially if you have a lot of assets, but you will probably get to keep your furniture and personal effects, your car and your business tools. You may not even lose your house. While a secured creditor has the right to repossess the security you gave them if you default on your contract, they can’t do this merely because you’ve gone bankrupt, as long as you have managed to keep up your payments. Another thing, if you are worried about being able to renew a mortgage don’t be. These things are usually done almost automatically and even if you are still in the bankruptcy when the renewal time comes people do not usually have a problem, especially with the banks.

4. I’ll take my spouse down with me.

Your spouse and their property should not be affected by your bankruptcy. Each person is responsible for their own debts. So if your spouse hasn’t co-signed a loan or guaranteed your debt, then they won’t be directly affected and their credit rating won’t be damaged. There may be indirect consequences, however. For example, your spouse may not qualify for a loan in future if your bankruptcy prevents you from being able to co-sign for it. But nowadays this is very, very rare. You can read more about the impact of bankruptcy on spouses here.

5. Bankruptcy will eliminate all my debts.

Hold on, cowboy. While bankruptcy will bring you considerable relief, no one can wave a magic wand and make everything go away (Although sometimes that’s what seems to happen.). Certain debts aren’t wiped out by your discharge from the bankruptcy. These include court fines, alimony, debts that were incurred fraudulently and any debts that you continued to pay after the bankruptcy started such as a mortgage, a car loans, etc. Then there are some student loans that you would be responsible for after your discharge.

All of these “myths” are misleading and can make a person shy away from seeing a trustee. Big mistake! Contact us and we will make sure you get correct information so you can determine what’s the right course for you; a bankruptcy, a proposal, or some other option. Only you can decide, so get the facts and then you’ll be able to make a good decision.

Is A Spouse Responsible For Credit Card Debt in Canada?

When it comes to marriage, a question may arise: Is a spouse responsible for credit card debt in Canada if the other spouse declares bankruptcy?

Sorry, Dear, I’m Bankrupt.

Nothing can make for a frostier breakfast conversation than revealing your financial woes have led to bankruptcy. Fueling the tension of guilt and anger is the fear one spouse filing for bankruptcy is going to drag down the other.

But if you do file for bankruptcy does this automatically affect your spouse?

The short answer is no. Each person is responsible for their debts. So if your spouse has not co-signed a loan or guaranteed your debt, then they won’t be directly affected and their credit rating won’t be damaged. There may be indirect consequences, however. For example, your spouse may not qualify for a loan in the future if your bankruptcy prevents you from being able to co-sign for it.

Don’t Give Credit Where it’s Due

But the truth is, married life can be complicated, with intertwined finances and joint ownership of assets. Take credit cards, for example. If your spouse has a joint or supplementary credit card – that is, one with their name but has the same account number as yours – then he/she would also be responsible for any debt.

On the other hand, if they have a supplementary credit card and have never used it, chances are they wouldn’t be responsible for the debt. The case could also be made that they are not saddled with the debt if they have only used the card occasionally, for small amounts.

However, if the two of you have used the cards extensively, you are both on the hook for the debt. This doesn’t change if only you go bankrupt. Things can get worse for your spouse because creditors can, and probably will, pursue them for the full amount of the money owed, and not just 50 percent. This scenario would be the same for any loan they’ve co-signed, such as a mortgage. (Though a legal case could be made that they are not responsible if they didn’t get legal counsel before co-signing the loan.)

Nothing Ruins a Good Divorce Like . . .

The risk of being saddled with joint debt seems to increase during divorce when communication and cooperation often dwindle. Some might be under the impression that debt is divided 50-50, as assets often are. But if one spouse files for bankruptcy, the other could be left responsible for the full debt and not just half, with avid creditors giving them their undivided attention.

Time to Take Out the Saw

Another consideration when one spouse goes bankrupt and the other is spared is jointly owned assets. That Harley and sidecar you both own for summer camping trips might need to be sold to pay what you owe to creditors. Your spouse’s portion of the motorcycle would be spared but you couldn’t exactly saw the vehicle in half.

Generally speaking, jointly owned assets have to be reviewed one by one by the trustee to see how they will be treated.

In summing up, if you not sure the answer the question “Is a spouse responsible for credit card debt in Canada?” or about other assets or liabilities, all the ins and outs of the effects of bankruptcy on a spouse need to be considered and explained by a licensed trustee.

Will I Lose My Home in a Bankruptcy?

The fear of losing your home is a powerful one. When their finances go south, many imagine that bankruptcy will leave them homeless. Is this fear justified? Not really, or not in the normal course of a bankruptcy.

The fear of losing your home is a powerful one. When their finances go south, many imagine that bankruptcy will leave them homeless. Is this fear justified? Not really, or not in the normal course of a bankruptcy.

Yes, when you go bankrupt, you give control of your assets to a trustee in exchange for getting rid of your debts. This, in theory, could mean that the house gets sold to help pay back the creditors. But in practice this rarely happens, mainly because it is not in the best interests of everyone involved. The trustee has a lot of discretion, which he or she generally uses to safeguard the rights and interests of both the creditors and the debtor. Selling the house outright usually doesn’t achieve this purpose. So what normally happens?

Well, there are many different scenarios. If you have no realizable equity in the house – equity is the amount you’d get selling the house after deducting the mortgage and other associated costs – there is no point in selling the house, because all the money would just go to pay off the mortgage(s). In this case you get to keep the house as long as you keep paying your mortgage. The trustee doesn’t get involved.

But, what if you did have some equity, say roughly $20,000? To keep the house, you would have to pay the trustee this amount, because that’s what the creditors would have received if the house had been sold. So the creditors end up getting their fair share and you keep your house.

Yes, but if you had $20,000 to throw around, you wouldn’t be bankrupt in the first place, right? Well, you would have to raise the money, but the trustee would work with you to accomplish this. For instance, you might be able to get the money through a second mortgage. Or you could work out a direct monthly payment plan with the trustee. In either case, you would keep your house.

Where things start to get more complicated is if you have a significant amount of equity in the home, let’s say $100,000. In order to hang onto the castle, you would have to pay the trustee 100 large – a whopping sum, but not impossible and financing is usually obtainable.

But, in such a case you probably would want to explore the legal alternative to bankruptcy: a consumer proposal. If you go this route, you don’t risk losing the house. You simply offer the creditors a settlement, negotiated by your trustee under the protection of the law. Most often this solution satisfies everyone because it pays the creditors an acceptable sum while allowing you to escape the debt quagmire in an orderly and manageable way: win-win.

There are a couple of other points to understand when you’re dealing with the house question.

The first is that in all these scenarios the trustee will remind you of your right to get advice from a lawyer of your choice, someone who is there to protect specifically your interests. This is your basic legal right, but it becomes much more important if you have a lot of equity in your home. A good lawyer will help you deal with the situation and probably get you a better deal from the trustee and creditors than if you were doing this on your own.

The second point is that you should ask yourself: Whether I go bankrupt or not, can I afford to keep the house? If I try to hang on to it will it just drag me back into debt trouble down the line?

This is a tough one. We tend to be emotionally attached to our house in a way that we aren’t with most other things, even our cars. But, we have to ask ourselves this question if we’re going to regain control of our finances. The trustee can help you better understand your situation, but the answer to this question can only come from you. And you need to be brutally honest with yourself about it.

So, to get back to the original question: “If I go bankrupt will I lose my house?” For most people (the vast majority) the answer is “No!” So don’t be afraid to consult a trustee because you’re worried about losing the house. Contact us and get the facts. Remember our TV commercial: “It may be the most stress-relieving call you ever make.”

Highway No Longer Takes Toll on Bankruptcy

The operators of Ontario’s Highway 407 Express Toll Route (ETR) can no longer arrange for vehicle permits to be withheld from bankrupt drivers, according to a recent Ontario’s Court of Appeal ruling.

The operators of Ontario’s Highway 407 Express Toll Route (ETR) can no longer arrange for vehicle permits to be withheld from bankrupt drivers, according to a recent Ontario’s Court of Appeal ruling.

A January 2nd Toronto Star article states, “A recent series of court battles have attempted to resolve a key question that pits federal legislation against provincial: if a driver doesn’t pay the 407ETR toll, should the province take away their licence?”

The provincial Highway 407 Act dictated that the answer was yes. If the drivers didn’t take care of their tolls then the highway company could contact the province, which would refuse to issue vehicle permits to the drivers until everything was paid up.

This would include people who were undergoing bankruptcy and sometimes owed tens of thousands of dollars to the toll highway. Feeling that this violated the “fresh start” principle of the Bankruptcy Insolvency Act (BIA), lawyers launched a class action suit on behalf of insolvent drivers denied vehicle licences despite being declared bankrupt.

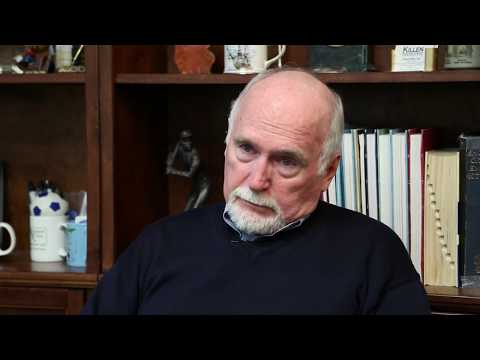

“As a trustee we had to tell people that though their future discharge would legally erase the debt, they would probably still have to pay the 407ETR debt or at least make a settlement with them if they wanted to license their car,” explains Richard Killen, president and trustee with Richard Killen & Associates. “There was nothing illegal about the 407ETR accepting a ‘voluntary’ payment from a discharged bankrupt. The Ministry of Transportation would then receive a notice from the 407ETR that the debt was paid and a licence would be issued. The circular argument made any effort to solve the problem an exercise in futility. The MOT simply shrugged and tossed the ball over to the 407ETR.”

He adds, “It took years for the Federal Office of the Superintendent of Bankruptcy to involve itself, and even that was only after a bankrupt pushed this challenge through the lower courts. This appellate decision pretty well puts to rest the whole question. Now we are in a position to tell people when they consult us that their debt to the 407ETR is as dischargeable as their debt to Visa. This is news.”

Consumer Proposal or Bankruptcy?

If you are coping with severe debt problems, you have five choices to deal with the crisis: Get a consolidation loan, try to negotiate with your creditors, run away, do a consumer proposal, or go bankrupt.

If you are coping with severe debt problems, you have five choices to deal with the crisis: Get a consolidation loan, try to negotiate with your creditors, run away, do a consumer proposal, or go bankrupt.

The first three options you can handle yourself (we don’t recommend trying to run from your problems; they have a nasty habit of catching up). Personal bankruptcies and consumer proposals are solutions governed by the Bankruptcy and Insolvency Act, and they can only be handled by Licensed Insolvency Trustees.

So why would you choose one of the legal solutions over the other? Well, every person’s case is different, so you need to come into a trustee to get advice tailored to your particular situation. But painting with broad brushstrokes, a bankruptcy is a faster and less expensive process, whereas a proposal may protect more of your assets and save your name from being associated with bankruptcy.

With a personal bankruptcy, you are released from your debts after you comply with certain duties. It’s a process that can be over in as little as nine months. Some of your assets would be exempt from this legal process – such as furniture and personal effects – and others would be handed over to the trustee and be used to repay creditors.

This latter category could include houses, high-worth cars, jewelry and certain RRSPs. Also, if you have an income over a certain set amount, you would have to pay 50% of this surplus to creditors, probably lengthening the time you were discharged from the bankruptcy.

A consumer proposal essentially reorganizes your debts. If the proposal is accepted by your creditors, you only have to make one manageable payment a month to the trustee. The length of term for a consumer proposal is five years or less, depending on fast you want to and are able to address your obligations. But generally speaking, it’s a longer more expensive process that a bankruptcy.

With the proposal you avoid the ‘stigma’ of bankruptcy and get to keep all your assets, providing you make your monthly payments and don’t slide into bankruptcy anyway. You may also want to consider a proposal if bankruptcy would also force your spouse to follow the same route, or if you are expecting to receive a large sum of money down the road.

Also, with a bankruptcy, you must complete a monthly budget for all income and expenses, as well as supply copies of your pay stubs to the trustee. If your income goes up during the period of your bankruptcy, then your surplus payments would also increase. With a consumer proposal, there are no monthly reporting requirements.

A New Problem for the Old

While aging baby boomers aspire to a placid retirement, this dream is being threatened by a growing problem: senior debt. An August 2013 article in Financial Post says, for example, “A report provided [by] ratings agency Equifax Canada shows average debt for consumers aged 65 and over climbed 6.5 per cent over the past year, the biggest year-over-year increase in the period for any age group.”

While aging baby boomers aspire to a placid retirement, this dream is being threatened by a growing problem: senior debt. An August 2013 article in Financial Post says, for example, “A report provided [by] ratings agency Equifax Canada shows average debt for consumers aged 65 and over climbed 6.5 per cent over the past year, the biggest year-over-year increase in the period for any age group.”

Apparently Canadians 65 and older account for eight per cent of bankruptcies, up from six per cent five years ago. “There’s been an increase since 1987 in bankruptcy of people over 65 of 3,900 per cent, it’s just huge,” says Nadim Abdo, vice-president of consulting and analytical services at Equifax.

Some reasons for this alarming situation include:

- People are living longer, so may not have saved enough money to cover their entire retirement.

- Parents are bailing out debt-ridden adult children.

- Seniors are sinking too much money into real estate, lured by low interest rates and the prospect of high returns.

- Widows or widowers don’t change their spending habits after a spouse dies and their pension disappears.

The results of this rising problem is not only the anxiety of dealing with creditors but the increased risk of health problems, such as rising blood pressure and heart attacks, and passing estates to heirs that have to be placed into bankruptcy because of crushing debt.

Will Bankruptcy Affect My Income?

Some people assume that if they file for bankruptcy they will have to turn over all their income to the trustee. Not true.

But there are other concerns people have over their income. A question we are often asked is: Will bankruptcy affect my income? Will I lose any of it to the trustee or creditors? The answer is: maybe, but probably not.

The fact is after going bankrupt people often find they now have “free income” for the first time in years. This is because they no longer have a long list of debts to pay every month.

When a person goes bankrupt, they are basically saying they can’t pay all their debts. They may be able to pay their rent and utilities and put food on the table, but they can’t do that and pay their credit cards and other loans. However, the moment they go bankrupt and get under the legal umbrella, those same creditors can no longer demand money from them, so they may actually have money to spare.

Now it is possible that person’s income maight be affected, but only if they are making such a substantial amount every month that, in fairness to the creditors, a portion of their surplus should be set aside for the creditors’ benefit. But this only applies after all the necessities are taken care of, so it is not such an onerous thing and most people have no problem with it. In fact it helps people feel better about having to go through the whole process in the first place.

There is actually a formula for working this out and the trustee will explain it all before you make the decision to file the bankruptcy. It’s just one of the many questions that a visit to the trustee clears up.

Most people don’t necessarily think of it this way, but the process goes directly to restore your control and give you an empowerment over your own affairs. This is one of the main goals and purposes of the bankruptcy laws.

The Road to Recovery

It was a perfect storm of personal and professional misfortunes. Bryan was a successful independent marketing communications consultant, well respected in the business with a good network of friends. But in his late 50s he discovered that he had adult attention deficit disorder (ADD), with a host of problems, ranging from an inability to focus to poor organization skills and depression. After years of laboured compensation for the symptoms, he felt the copying structure he had carefully built begin to fall apart.

It was a perfect storm of personal and professional misfortunes. Bryan was a successful independent marketing communications consultant, well respected in the business with a good network of friends. But in his late 50s he discovered that he had adult attention deficit disorder (ADD), with a host of problems, ranging from an inability to focus to poor organization skills and depression. After years of laboured compensation for the symptoms, he felt the copying structure he had carefully built begin to fall apart.

Then he lost his biggest client. With the onset of a deep depression, he found it harder and harder to do work and make up for the lost income. He started to drain his savings and line of credit to stay afloat.

He took a consolidation loan. The Canadian Revenue Agency called about missed tax installment payments. He had to ask for a personal loan from a friend to pay for a month’s apartment rent. He spent a Christmas without money to buy presents. He missed a bank loan payment.

“It was the lowest ebb in my life. I felt like a complete failure,” says Bryan in his quiet voice. “My parents were alive at that point. They berated me for my financial mismanagement. My father had been a bank manager. He told me that if I went bankrupt I would never be able to get credit again.”

With this sword hanging over his head, and not much hope to propel him forward, Bryan went to an assessment with Richard Killen. He may have gone into the meeting with intense sense of “embarrassment” at winding up in this precarious financial position, but he was soon reassured to learn that his problems were manageable.

After a detailed evaluation of his situation and going through the ins and outs of a consumer proposal versus a bankruptcy, Bryan felt the latter would best suit his situation. The instability of his income at the time would have made it difficult to commit to the monthly payments a consumer proposal would demand. But the most important thing was that the decision was his to make. This helped put him back in control of his financial life – a luxury he had not experienced in a long time.

Almost immediately Bryan felt a surge in spirits knowing that the burden of debt would be lifted. “It was this huge sense of relief,” he recalls. “I was told by Howard that when the phone rings, just to give them his name and number, and he would take it from there. When the bank called the next week, they were very matter of fact and nice about it when I told them. It was just business for them.”

Filing for bankruptcy in 2003, Bryan was able to keep his car, since he used it for work purposes, as well as his personal assets. And he didn’t have to pay any portion of his income to creditors, since it fell under the legal threshold set in the Bankruptcy and Insolvency Act.

During the bankruptcy, he attended the mandatory credit counselling sessions held at Richard Killen & Associates. At the same time, he underwent treatment for his ADD, getting it under control with therapies that included learning the complex body motions of the martial arts.

Nine months after filing for bankruptcy Brian was discharged and able to make his life anew. What about his father’s dire prediction that he would never get credit again? “Evenbefore I was discharged, credit card companies were calling me and offering me credit. I applied for a Royal Bank Visa after discharge and have never missed a payment,” he says.

Since then, Bryan has gone from strength to strength in his life. The return of his self-esteem has enabled him to rebuild his business. He has co-founded a company that will create a smartphone app to help kids with ADD. He is poised to take his third-degree black exam in karate. He has downsized and simplified his life to better protect him from financial vagaries and to minimize the disorganization associated with ADD.

Bryan adds with pride, “It’s a great feeling to get your life back and become a fully contributing member to society again.”

Contact Richard Killen

FREE No Commitment Consultation

Contact us now for a fresh start!

“Serving Toronto & the GTA for over 25 years.”

Recent Blog Posts

- Debt Repayment vs Vacation: How to Balance Fun and Financial Freedom

- Job Loss & Debt in Canada: How a Licensed Insolvency Trustee Can Help You Regain Control

- CRA Debt Canada: Why Waiting Until September Costs You More

- Summer Vacation on Credit? What a Licensed Insolvency Trustee Wants You to Know About Vacation Debt in Canada

- The Canada Groceries and Essentials Benefit 2026: What It Means for Your Budget and Debt