Cheap Summer Fun in Toronto

We all like to take nice summer vacations. But long car trips, travel abroad, cottage rentals and even camping can strain the pocketbook. If you are trying to save money this summer, why not stay in the city and enjoy some of its pleasures?

We all like to take nice summer vacations. But long car trips, travel abroad, cottage rentals and even camping can strain the pocketbook. If you are trying to save money this summer, why not stay in the city and enjoy some of its pleasures?

Yes, Toronto has lots of pricey entertainment options. But it also provides many inexpensive and free choices for the budget conscious. For example, you can enjoy:

Cheap Shakespeare

For yet another summer Canadian Stage presents its popular Shakespeare in High Park series. To take in the Bard under the stars with a blanket and picnic, you can pay what you like at the gate or reserve tickets online. This year the lighthearted As You Like It and the intense Titus Andronicus are performed on alternate nights. Gates open at 6 p.m. and the plays start at 8 p.m.

Cheap Laughs

Toronto has its share of inexpensive standup and sketch comedy and improv nights. Here is a listing of some of best places to get a laugh in the city, ranging from stalwarts like Yuk Yuks and Second City to up-and-comers that include the Rivoli and Black Swan.

Cheap Board Games

Like to play games? Good, go to the Snakes and Lattes Board Game Café, where you’ll pay a paltry $5 cover charge, order something to drink (for as little as $2) and the pick a game from the more than 2,300 choices that line the shelves. Don’t know what to play? Then ask one of the café’s “Game Gurus.” As its site explains, they “are like wine sommeliers. Not only will they try to help find you the right game for your group, they’ll go on and explain how it’s played.”

Cheap Drinks

Drinking at bars can be an expensive pastime. Thank goodness for Nirvana . . . as well as other cheapo swilleries such as The Rhino, Einstein’s and Java House. Yes, you’ll find $10 jugs of draft, two-for-one specials, $3 mixed drinks and more. You will also save on gas, because you should drive to these high-volume, low-cost joints, which are listed here.

Cheap Movies

Not just cheap but free. Toronto has an abundance of outdoor venues to enjoy film screenings, ranging this summer from Les Vacances de Monsieur Hulot to The Adventures of Priscilla, Queen of the Desert. Venues range from Harbourfront to Yonge-Dundas Square to Christie Pits.

It’s the Little Savings That Count

We all know about the big buys that do damage to our bank accounts: homes, cars, vacations, etc. But equally insidious are the small regular purchases that we don’t really notice but add up over time, whether it’s expensive designer coffee or unused gym memberships. Here are five things you can do without, or with less of, to plump up the pocketbook.

1. Stop Going to Coffee Shops

Do you get a nice coffee from Starbucks or Timmy Ho’s everyday before getting down to work? You can be spending a couple of bucks a day or much more if you are getting some of the premium coffee-based drinks. For less than you spend in a month in coffee shops you can get your own coffee machine at home (for under $20 at the low end!) and a pound of something fair trade and delicious. That way, when you treat yourself out, it is a treat and not part of the daily grind of starting your heart for work.

2. Give up Your Gym Membership

Lots of us have unused gym memberships, meaning we’re paying hefty monthly fees for no reason. So give it up. This is not to say you should give up exercise. Do more at home. Take up walking or bike riding and, if you live close enough, bike it or hoof it to work, saving big bucks on the gas and parking of a car commute. If you like to do your aerobics or Pilates in a group, check out the local rec or community centre, where classes may be cheap or even free.

3. Stop Impulse Buying

If you’re thinking about buying something you’re not sure that you really need, make yourself wait 30 days before making the purchase. Often the impulse will pass. Or if you’re in a store shopping and see something you want to buy on the spur of the moment, circle way and wait 20 minutes before picking it up. Your consumer desire may wane. And when grocery shopping, make a list and stick to it. Yes, the tub of Häagen-Dazs may be half price but it doesn’t save you money if you weren’t planning t0 buy it in the first place.

4. Save Money on Your Entertainment Media

Spending too much on your cable TV package and pay per view? Then downgrade or eliminate your service and get movies and TV shows through low-cost services like Netflix and Redbox. Or better yet read a book. Don’t buy a book but go to your library and take one out. It’s free. You can also take out movies and even put a dent in your iTunes habit by renting CDs of music that you can rip to your MP3 player (ask your kids how).

5. Check Your Phone Plan

If you have a cellphone, check your usage to see if your plan is the most economical one for you. Also, since signing on, the phone company may have introduced lower priced plans, with unlimited Canada-wide calling for example, that they are in no hurry to tell you about. And you may be able to negotiate lower rates than the ones offered. But don’t do this at the phone company’s retail shop. They have to stick to the listed prices. Call your phone company, make noises about quitting and when they pass you on to their retention expert, swoop in and make a deal, citing the low prices to be had elsewhere (do your research). Also, if you don’t use your cellphone much, consider switching to a pay-as-you go plan. And finally, if you have both a cellphone and landline, get rid of one. Just because you grew up with a rotary phone doesn’t mean you need one now.

There are probably many other things going on in your life that drain your financial resources without giving you much (or any) value in return. Sit down and make an inventory. You’ll very likely shock yourself. Remember, you are supposed to be in charge of your life, not Starbucks.

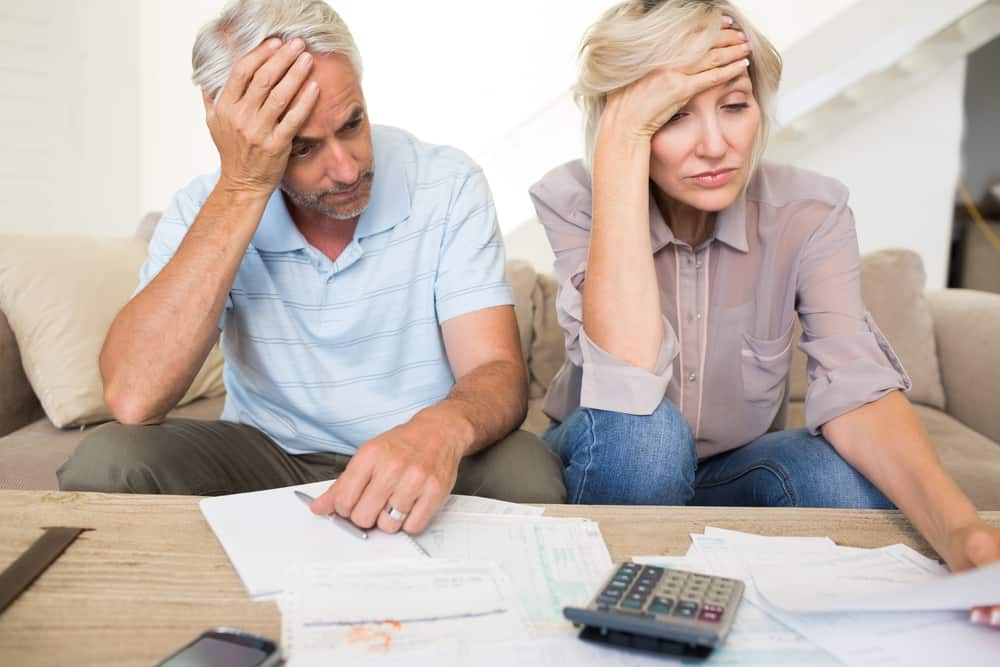

Pre-Retirement Canadians Embrace Mortgage Debt

People looking forward to retirement usually try to retire their debts first, especially their mortgages, so they can enjoy their leisure without financial worries. But a story in the Globe and Mail reveals that more and more Canadians are going into their golden years with a substantial financial burden.

People looking forward to retirement usually try to retire their debts first, especially their mortgages, so they can enjoy their leisure without financial worries. But a story in the Globe and Mail reveals that more and more Canadians are going into their golden years with a substantial financial burden.

“Pre-retirement Canadians in the their 50s are taking on an alarming amount of debt and are most at risk of bankruptcy,” says April Dunn, owner of the Red Door Mortgage Group in Vancouver, citing a new study that examined about 7,000 insolvency filings. She reveals in the Globe interview that about half of all retired people in this country are carrying debt, “with many stuck managing two or more payments a month.”

Even so, not all of these people are getting into debt as a desperate measure. Some want to free resources for other uses and believe they have the wherewithal to manage their debt. Others are seeking to take advantage of historically low interest rates, or they are leveraging their property to pass money to their kids, so they can perhaps buy their own homes.

How Much Is Too Much?

People sometimes ask: “If I go bankrupt will the trustee take all my income?” Well the simple answer is NO. But to understand that answer you need to wade through some layers of legal complexity.

People sometimes ask: “If I go bankrupt will the trustee take all my income?” Well the simple answer is NO. But to understand that answer you need to wade through some layers of legal complexity.

While you go through bankruptcy, the trustee is required to monitor your income to see if maybe some part of it should go to your creditors. Remember, you have stopped making any payments directly to those creditors, so they are not getting anything from you. But, assuming you’re working and have income, it’s fair to ask whether any portion of your income should go to the creditors.

In the old days this question had to be answered by the court on a case-by-case basis. But since the early 1990s, the courts couldn’t keep up with the rising number of bankruptcies, so the government decided to let the trustee handle this question. After all, the trustee takes care of practically everything else. However, to ensure that consistency and fairness is maintained across the country, the government gave the trustees a strict formula that enables them to work out a solution that is fair and protects both your rights and your creditors’.

Every year, using the latest cost of living statistics, the federal government sets a “Standard” based on how many people live in a household. (Obviously the more people in the house, the more money these people need to get by.) This standard establishes a threshold. If your family income exceeds the applicable threshold, you are deemed to have “Surplus Income.” If you have a surplus, you may pay half the amount to a trustee for the benefit of the creditors. The formula is fair and most people have no problem with it.

Here’s an example: You’re part of a family of two who has a total combined after-tax income of $2,908. This is exactly $400 more than the standard threshold for a two-person family ($2,508). So the bankruptcy law requires you to pay half of this $400 surplus income, $200, to the trustee for the creditors. The Industry Canada website has all the details.

While this formula is fair, it can get complicated, especially since everyone’s situation is different. For instance, you have the right to question and disagree with whatever number the formula comes up with. There is a mediation procedure in place that can help you to work out a compromise.

Since the issue of surplus income may affect your decision about what course to take to solve your debt problems, you need to know the facts and your options. The best way to do this is have a trustee at Richard Killen & Associates explain them to you. It doesn’t matter how much surplus income you may or may not have, the consultation with us is truly FREE.

Five Ways to Rebuild Your Credit

You’ve gone through a bankruptcy and you want to get your life back to normal as fast as possible. While it won’t happen automatically and you will have to be proactive about it, you can actually take steps to start repairing your credit rating right away – as soon as you’re discharged. Here are five ways to do it:

You’ve gone through a bankruptcy and you want to get your life back to normal as fast as possible. While it won’t happen automatically and you will have to be proactive about it, you can actually take steps to start repairing your credit rating right away – as soon as you’re discharged. Here are five ways to do it:

Speak to Your Bank Manager: They are a good source of information to get you started on the road to credit repair. In most cases they are also quite supportive.

- Start Saving: Creditors like to lend to people who don’t really need the money. So use your savings account or open one if you don’t have it. Every pay period, put in a small amount in the account, perhaps arranging for an automatic withdrawal. Or if you were used to paying the trustee a certain amount each month during the bankruptcy process, just continue to put the same money in your savings account. By the end of the year you would have a nice balance in the account, sure to impress creditors. (This is called paying yourself.)

- Get a Secured Credit Card: This type of credit card is secured by a deposit account that you own. So if you can scrape together, say, $500, you can use that as a deposit with the credit card company and get a $500 limit on a new credit card. You would still have to make regular payments on it every month like a regular credit card. If you keep this card in good standing it will all count towards rebuilding your credit rating.

- Pay Your Bills on Time: Pay all your bills, including utilities and credit cards, promptly. Creditors like to get paid on time. Some people are under the misapprehension that if they carry a balance on their credit card from month to month then that will endear them to the credit card company and boost their rating. Not so. It just costs you money.

- Get a Copy of Your Credit Report: There are two main Canadian credit bureaus, Equifax Canada and TransUnion Canada. This is where all your credit information is stored. You are entitled to get a copy of your credit report. Get it. You can see if there are any mistakes and correct them. You also have the option of putting in a short note that will be given out to anyone who collects a credit report on you.

Is A Spouse Responsible For Credit Card Debt in Canada?

When it comes to marriage, a question may arise: Is a spouse responsible for credit card debt in Canada if the other spouse declares bankruptcy?

Sorry, Dear, I’m Bankrupt.

Nothing can make for a frostier breakfast conversation than revealing your financial woes have led to bankruptcy. Fueling the tension of guilt and anger is the fear one spouse filing for bankruptcy is going to drag down the other.

But if you do file for bankruptcy does this automatically affect your spouse?

The short answer is no. Each person is responsible for their debts. So if your spouse has not co-signed a loan or guaranteed your debt, then they won’t be directly affected and their credit rating won’t be damaged. There may be indirect consequences, however. For example, your spouse may not qualify for a loan in the future if your bankruptcy prevents you from being able to co-sign for it.

Don’t Give Credit Where it’s Due

But the truth is, married life can be complicated, with intertwined finances and joint ownership of assets. Take credit cards, for example. If your spouse has a joint or supplementary credit card – that is, one with their name but has the same account number as yours – then he/she would also be responsible for any debt.

On the other hand, if they have a supplementary credit card and have never used it, chances are they wouldn’t be responsible for the debt. The case could also be made that they are not saddled with the debt if they have only used the card occasionally, for small amounts.

However, if the two of you have used the cards extensively, you are both on the hook for the debt. This doesn’t change if only you go bankrupt. Things can get worse for your spouse because creditors can, and probably will, pursue them for the full amount of the money owed, and not just 50 percent. This scenario would be the same for any loan they’ve co-signed, such as a mortgage. (Though a legal case could be made that they are not responsible if they didn’t get legal counsel before co-signing the loan.)

Nothing Ruins a Good Divorce Like . . .

The risk of being saddled with joint debt seems to increase during divorce when communication and cooperation often dwindle. Some might be under the impression that debt is divided 50-50, as assets often are. But if one spouse files for bankruptcy, the other could be left responsible for the full debt and not just half, with avid creditors giving them their undivided attention.

Time to Take Out the Saw

Another consideration when one spouse goes bankrupt and the other is spared is jointly owned assets. That Harley and sidecar you both own for summer camping trips might need to be sold to pay what you owe to creditors. Your spouse’s portion of the motorcycle would be spared but you couldn’t exactly saw the vehicle in half.

Generally speaking, jointly owned assets have to be reviewed one by one by the trustee to see how they will be treated.

In summing up, if you not sure the answer the question “Is a spouse responsible for credit card debt in Canada?” or about other assets or liabilities, all the ins and outs of the effects of bankruptcy on a spouse need to be considered and explained by a licensed trustee.

Contact Richard Killen

FREE No Commitment Consultation

Contact us now for a fresh start!

“Serving Toronto & the GTA for over 25 years.”

Recent Blog Posts

- Debt Repayment vs Vacation: How to Balance Fun and Financial Freedom

- Job Loss & Debt in Canada: How a Licensed Insolvency Trustee Can Help You Regain Control

- CRA Debt Canada: Why Waiting Until September Costs You More

- Summer Vacation on Credit? What a Licensed Insolvency Trustee Wants You to Know About Vacation Debt in Canada

- The Canada Groceries and Essentials Benefit 2026: What It Means for Your Budget and Debt